Water mitigation stops damage in its tracks after water invades your home. In the first critical hours upon discovering water damage, stopping the damage before it spreads helps to protect both your home and insurance claim.

Key takeaways:

- Water mitigation is the process of stopping active water damage, which involves drying affected areas and preventing secondary damage after leaks, floods, or plumbing failures.

- Mitigation comes before restoration and can affect the outcome of your insurance claim.

- Insurers may deny coverage for mold or rot if the homeowner fails to take reasonable steps.

What Is Water Mitigation?

Water mitigation refers to the steps taken by the insured to minimize the loss or damage to the insured property. This process is based on the premise that the insured has a responsibility to take reasonable and necessary steps to prevent or reduce the loss or damage to the insured property. The goal is to control moisture fast, stabilize the environment, and prevent secondary damage.

Why Water Mitigation Is the First Step After Water Damage

Water mitigation comes first because water damage escalates fast, often within hours. Moisture migrates through drywall, insulation, framing, and flooring, creating hidden damage long before stains or warping appear, such as mold growth and structural weakness.

This process begins by stopping the source of water, extracting standing moisture, and drying affected materials. From there, technicians monitor humidity levels and material moisture until conditions return to safe ranges. These actions limit how far water travels inside behind walls and under floors, where hidden damage often develops.

Mitigation does not rebuild damaged areas. It stabilizes the structure so restoration work can proceed safely and efficiently, without surprise mold or structural issues surfacing later.

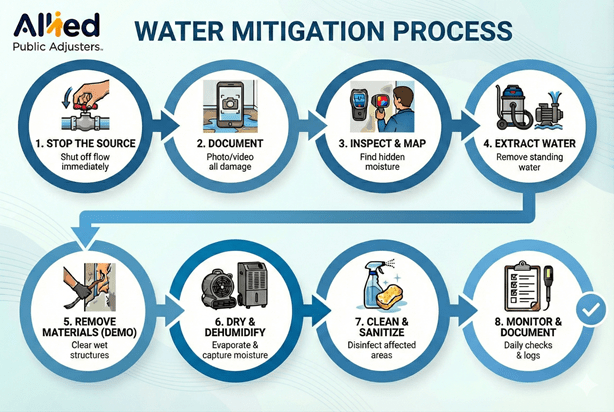

A Step-by-Step Explanation of the Water Mitigation Process

Professional water mitigation follows a structured sequence designed to contain damage, stabilize materials, and document conditions for insurance purposes. Each step builds on the last, creating a controlled drying environment that limits further loss.

1. Stop the Water Source

First, isolate broken pipes if it’s safe to do so, shut off main lines, seal roof penetrations, or contain exterior intrusion. If there’s any chance of water reaching electrical outlets or the breaker panel, call a technician.

2. Document Everything

Before moving a single wet item, document the scene. Take photos and videos of standing water, damaged materials, and affected areas. These records become evidence that could support a public adjuster in building your insurance claim.

3. Professional Inspection and Moisture Mapping

A professional inspection uses infrared cameras and moisture meters to map the full extent of the damage behind your walls and under floors. This data determines whether you need a simple dry-out or structural demolition.

4. Emergency Water Extraction

Technicians use industrial-grade pumps and wet vacuums to remove standing water from floors and carpets. This prevents the water from wicking up into the drywall and saturating the subfloor.

5. Selective Material Removal

You cannot dry a wall that is packed with wet insulation. Professionals must remove materials that are saturated beyond repair (such as carpet padding, baseboards, and lower sections of drywall) to expose the framing. This allows air to reach the wet structure and prevents mold from growing inside the cavities.

6. Drying and Dehumidification

Once the wet materials are gone, the drying begins. Professionals use industrial air movers to evaporate moisture and commercial dehumidifiers to pull the moisture out of the air. They run continuously to bring humidity down to a safe level.

7. Cleaning and Sanitization

After the structure is dry, affected areas must be thoroughly cleaned and sanitized. This step is mandatory for Category 2 (grey) and Category 3 (black) water. Engage professional contractors who use antimicrobial treatments and specialized tools to disinfect the property thoroughly and ensure the home is safe for reconstruction.

8. Monitoring and Documentation

Throughout the water mitigation process, technicians will typically track daily moisture readings and humidity levels. These daily logs verify that the drying is working and prove to the insurance company that you have fulfilled your duty to mitigate the damage.

How Water Damage Mitigation Prevents Secondary and Hidden Damage

Water damage mitigation is essential in preventing secondary losses because uncontrolled moisture can compound repair costs and health risks. A leak from an upstairs bathroom can travel into wall cavities, ceiling voids, insulation layers, and electrical pathways before visible signs appear.

This secondary damage can be more costly and difficult to resolve than the initial water intrusion, and may lead to insurance disputes. Rapid mitigation limits the damage by drying materials before moisture migrates deeper into your property structure.

Primary damage comes from the water itself. Secondary damage comes from what happens when water sits too long and can cause:

- Mold colonization

- Structural weakening

- Material degradation

- Indoor air contamination

The Centers for Disease Control and Prevention (CDC) warns that prolonged dampness increases respiratory risks, particularly for individuals with asthma, allergies, or compromised immune systems.

How Water Mitigation Impacts Insurance Claims

Most homeowners insurance policies include a clause that requires you to protect your property from further damage upon discovery. Failing to mitigate gives your insurer grounds to deny coverage for preventable secondary damage.

You can prove to the insurance company that you’ve acted responsibly by addressing water damage promptly. Thorough documentation of the mitigation process, including photographs, moisture readings, and itemized lists of damaged items, gives your claim strong backing and protects you if an insurer disputes that the damage was gradual or due to a lack of maintenance.

Water Mitigation Services vs. Restoration

Water mitigation services stabilize the damage in the first 24-48 hours through emergency extraction, demolition, and drying. The water damage restoration process happens afterward and includes rebuilding like replacing drywall, installing new flooring, and repainting. The scope of restoration can only be known after mitigation.

Misunderstandings often come from assuming mitigation includes restoration because the same company does both or says they handle everything. Most restoration companies offer both mitigation and restoration, but they’re separate scopes of work billed separately.

| Water Mitigation Services | Restoration Services | |

|---|---|---|

| Primary Goal | Stop active damage progression and prevent further loss | Repair and rebuild to return property to pre-damage conditions |

| Timeframe | Immediate. Within 24 to 48 hours | Scheduled after mitigation completes |

| Timeline | 3 to 7 days | Weeks to months depending on damage extent |

| Focus |

|

|

| Insurance Coverage | Usually covered under mitigation clause | Generally covered based on policy limits and deductibles |

What Is a Water Mitigation System?

A water mitigation system is a set of equipment and controls installed in (or around) a property to detect, contain, divert, or stop unwanted water before it causes damage.

Modern systems include leak sensors and automatic shut-off valves that detect abnormal water flow and stop supply lines before flooding spreads. IoT-based loss prevention systems, like smart water sensors, alert you to leaks early. And, when paired with an automatic shutoff valve, can stop the water supply to limit damage.

These tools can help reduce damage, but it won’t automatically make a claim easy. Coverage still depends on the cause of the loss and what your policy covers.

Common Types Installed in Homes

Leak Detection and Automatic Shutoff

Sensors installed near water heaters, under sinks, and behind toilets monitor for leaks. When they detect water or abnormal flow patterns, a smart valve closes the main supply line automatically.

Sump Pump Systems

These systems collect groundwater in a basin and pump it away from your foundation. Some models include battery backup to keep working during power outages.

Drainage and Grading

French drains, yard channels, and extended downspouts redirect water away from your foundation. Proper grading ensures water flows away rather than pooling against basement walls.

Backwater Valve

These prevent sewage from reversing direction and entering your home during heavy storms or when municipal systems get overwhelmed.

Roof Flashings and Temporary Barriers for Storm

Storm protection systems include properly maintained flashings around chimneys, vents, and roof penetrations that prevent water intrusion during severe weather.

Equipment Used by Professionals

Extraction Tools

Submersible pumps remove standing water from basements and crawl spaces while truck-mounted extractors pull water from carpets and padding. Wet vacuums handle smaller volumes in tight spaces where larger equipment won’t fit.

Drying Equipment

High-velocity air movers create airflow across wet surfaces to accelerate evaporation while industrial dehumidifiers pull moisture from the air for optimal drying conditions. Specialized drying systems target hardwood floors and wall cavities.

Containment and Environmental Control

Plastic barriers isolate affected areas to prevent contamination spread. Negative air machines create controlled airflow when dealing with contaminated water. HEPA filtration removes airborne particles during the drying process to protect occupants.

Moisture Meters and Monitoring Documentation

Moisture meters track drying progress in materials. Infrared cameras detect temperature variations caused by moisture, which may go undetected by the naked eye. All these are documented in monitoring logs to prove drying progress to insurance companies.

What Homeowners Should Know About the Cost of Water Mitigation

Water mitigation costs vary depending on the category of water damage and the size of the affected area. The price reflects the cost of specialized labor, equipment rental, and the emergency nature of the work.

The financial gap between immediate mitigation and delayed response often reaches five figures. The Insurance Information Institute reports that the average water damage insurance claim exceeds $15,000, driven largely by secondary damage that develops when moisture remains untreated.

A plumbing insurance claims public adjuster can be very helpful in ensuring you have taken all steps necessary for a fair payout.

Factors That Affect Water Mitigation Costs

Category of Water Damage

The IICRC classifies water damage into three categories based on contamination level.

| Category of Water Damage | Average Price Range | Impact |

|---|---|---|

| Category 1 (Clean) | $3.50 per sq. ft. | Easiest to dry and lowest risk |

| Category 2 (Grey) | $5.25 per sq. ft. | Requires sanitization of materials |

| Category 3 (Black) | $7.50 per sq. ft. | Requires full removal of porous items |

Size of the Affected Area

A bathroom overflow affecting 200 square feet costs less than a basement flood covering 1,500 square feet. More area means more equipment, longer drying times, and higher labor costs.

Materials

Water on tile floors extracts and dries faster than water in carpeted rooms. Hardwood floors might need specialized drying systems.

Speed of Mitigation

Delayed mitigation allows water to spread and penetrate deeper into materials. What starts as surface extraction becomes wall cavity drying. What could have been carpet cleaning becomes carpet replacement plus subfloor treatment.

Labor

The hourly rates of technicians and the number of personnel required for the job contribute a significant portion of the expense.

When To Seek Help With a Water Damage Insurance Claim

If you’re feeling overwhelmed, uncertain, or your insurance provider delays or denies you compensation, that is when you should seek help with a water damage insurance claim. Insurance company adjusters have a mandate to minimize the company’s financial exposure.

A public adjuster works for you instead. We investigate losses, document every area of damage, and advocate for the full benefits your policy should provide.

Common Challenges in Water Damage Claims

According to the Insurance Information Institute, water damage is the second most common insurance claim nationwide from 2019-2023. However, it is often the primary source of disputes, as insurers frequently use the gray area between sudden accidents and long-term maintenance to deny coverage.

Here are the common challenges homeowners face:

- Wrongful Denials: Insurers deny claims for various reasons, including late reporting, lack of maintenance, excluded perils, or policy lapses.

- Lowball Offers: The settlement offer seems too low to cover all repairs, replacements, and other associated costs.

- Delays: The insurance company takes an extended time to respond, process, or pay your claim, slowing your recovery efforts.

- Confusing Fine Print: Insurance policies include complex clauses, such as mold sub-limits and exclusions for continuous leakage, making it challenging to know exactly what you are owed.

- Disagreements on Damage: The biggest conflict is usually repair vs. replace. The insurer may offer to just dry and paint a wet wall, while the IICRC S500 standard requires verifying that the internal structure is dry. If it cannot be dried, it must be removed.

Standard homeowners policies cover internal plumbing failures but almost always exclude flood damage caused by rising water from outside (like rain or rivers). These require a separate flood policy. If you are dealing with external water intrusion, a flood damage insurance claim specialist can help you evaluate those specific coverage limitations.

How Claim Advocacy Helps After Mitigation

After the mitigation phase, the challenge shifts to securing funds for the full restoration. A water damage public adjuster prepares an evidence-driven claim package that includes the mitigation team’s drying logs, contractor bids, and forensic moisture maps. This comprehensive documentation makes it much harder for the insurance company to dispute the necessity of the repairs.

Allied Public Adjusters advocate for maximum payout based on your policy’s actual coverage. We work with your mitigation contractors to ensure proper documentation and handle negotiations while you focus on getting back to normal.

If you’re facing a complex claim or looking to maximize your insurance payout, schedule your free consultation today or call (949) 520-1390.

FAQs

What is the difference between water restoration and water mitigation?

Mitigation stabilizes damage through drying and water removal. Restoration rebuilds damaged materials, including drywall, flooring, and finishes.

Why is water mitigation important for insurance claims?

Your insurance policy requires you to prevent further damage after a covered loss. Proper mitigation fulfills this duty, supports your claim with documentation, and prevents secondary damage that insurers might not cover if you delayed response.

How soon should water mitigation begin after a leak?

Immediately. Mold growth starts within 24 to 48 hours of water exposure. The faster you begin extraction and drying, the less secondary damage occurs and the lower your total claim costs.

Does insurance require water mitigation?

Yes, most homeowners insurance policies include a clause requiring policyholders to take reasonable steps to mitigate damages after an event. Failing to do so can negatively affect your claim payout or lead to denial.

What happens if water mitigation is delayed?

Delays can lead to toxic mold, structural failure, and the denial of your insurance claim due to property neglect.

Is water mitigation covered by insurance?

Most homeowners insurance policies cover water mitigation expenses when related to a covered peril, such as a sudden burst pipe or accidental overflow. However, policies typically exclude damage from floods or gradual leaks due to poor maintenance.